Save money with the best balance transfer credit cards for good credit. Discover the top 5 cards with 0% intro APR periods and no balance transfer fees.

If you have good credit and want to save money on interest by transferring balances from high-APR credit cards, there are several excellent balance transfer card options to consider. The best balance transfer credit cards offer 0% intro APR periods along with no balance transfer fees.

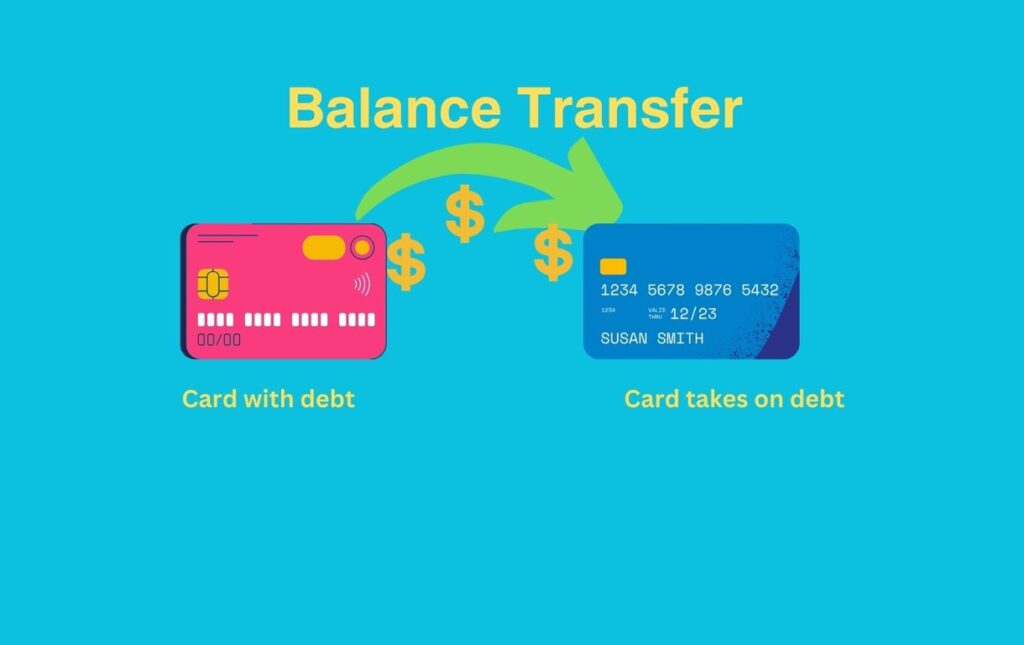

What is a Balance Transfer and How Does it Work?

A balance transfer allows you to move an existing balance from a credit card with a higher interest rate to one with a lower interest rate, ideally 0%. Many credit card companies offer promotional 0% introductory APR periods specifically for balance transfers.

Here's a quick rundown of how balance transfers work:

- You open a new credit card that offers a 0% promotional APR for balance transfers

- You request to transfer a balance from another existing credit card to the new card

- The credit card company pays off the balance on the other card and transfers it to the new card

- You pay 0% interest on the transferred balance for the promotional time period (typically 12-21 months)

Balance transfers allow you to reduce interest charges so more of your payments go toward paying down the existing principal balance. Just make sure to pay off the entire transferred balance by the end of the 0% intro period to avoid deferred interest.

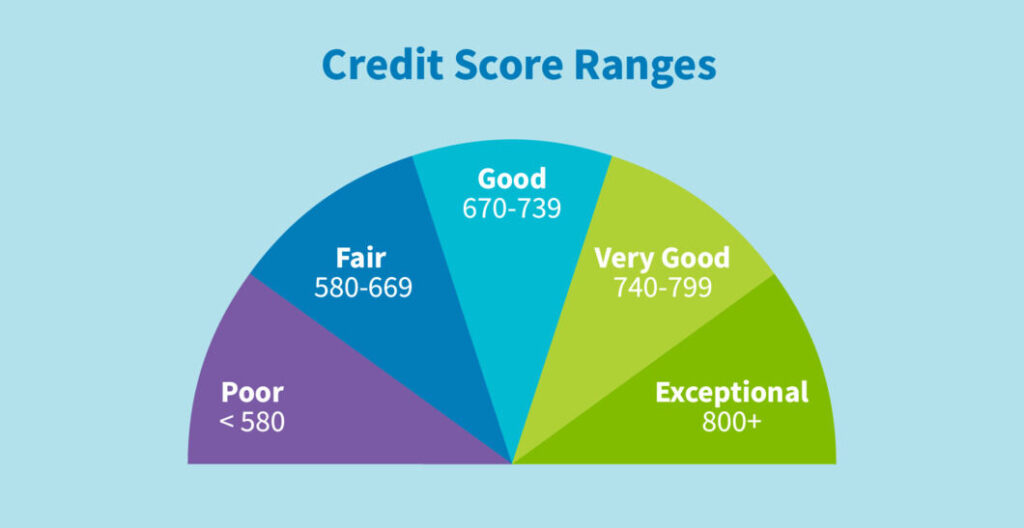

What is Considered Good Credit?

Good credit typically means you have a credit score in the 670-739 range, according to the FICO and VantageScore scoring models used by lenders. If your score falls within this range or higher, you'll qualify for the best balance transfer offers.

Having good credit demonstrates to lenders that you responsibly manage debt and make on-time payments. As a result, you may qualify for lower interest rates and better card terms compared to someone with fair credit or limited credit history.

Factors That Impact Your Eligibility

When applying for a balance transfer credit card, issuers will evaluate additional factors beyond your credit score to decide if you qualify, including:

- Credit utilization ratio - The percentage of your available credit that you currently have in balances. Aim for less than 30%.

- Length and consistency of credit history - How long you’ve actively used credit accounts.

- Mix of credit types - Having experience managing different types of credit like credit cards, auto loans, mortgages, etc.

- Recent credit applications - Applying for a lot of new credit at once can be a red flag for lenders.

Even with good credit, these factors could impact your approval odds or influence your credit limit. Maintaining healthy credit habits helps ensure you remain eligible for top card offers.

The Top 5 Balance Transfer Credit Cards for Good Credit

Based on a long intro 0% APR periods and no balance transfer fees, here are the top five balance transfer cards currently available for applicants with good credit:

1. Wells Fargo Reflect Card

- 0% Intro APR: 0% for 21 months on purchases and balance transfers

- Balance Transfer Fee: None

- Perks: No annual fee or foreign transaction fees

The Wells Fargo Reflect card stands out for its exceptionally long 21-month 0% intro period on both new purchases and balance transfers. This makes it one of the best balance transfer cards if you need more than 12-15 months to pay off a transferred balance without interest.

2. Citi Diamond Preferred Card

- 0% Intro APR: 0% for 21 months on balance transfers

- Balance Transfer Fee: 5% of each balance transfer ($5 minimum)

- Perks: No annual fee or foreign transaction fees

While it charges a small balance transfer fee, the Citi Diamond Preferred card matches the 21-month intro period offered by the Wells Fargo Reflect. Between these two cards, you’ll find some of the longest 0% term durations currently available.

3. U.S. Bank Visa Platinum Card

- 0% Intro APR: 0% for 20 billing cycles on balance transfers

- Balance Transfer Fee: None

- Perks: No annual fee or foreign transaction fees

With no balance transfer fees and a generous 20-month intro 0% term, the U.S Bank Visa Platinum card is another leading choice if your focus is saving on interest. After the intro rate ends, a competitive 14.99% fixed APR applies.

4. BankAmericard credit card

- 0% Intro APR: 0% for 18 billing cycles on balance transfers

- Balance Transfer Fee: 3% ($10 minimum)

- Perks: No annual fee or foreign transaction fees

Though not as long as other offers on this list, Bank of America provides an solid 18-month 0% intro period for new balance transfers. It does charge a small 3% fee but there is no annual fee.

5. Wells Fargo Active Cash Card

- 0% Intro APR: 0% for 15 months from account opening on purchases and qualifying balance transfers

- Balance Transfer Fee: Up to 5% ($5 minimum)

- Perks: $200 cash rewards bonus after spending $1,000 in purchases in the first 3 months and 2% cash back on all purchases

The Wells Fargo Active Cash card combines a competitive 15-month 0% intro offer with the opportunity to earn unlimited 2% cash rewards on purchases. There is a balance transfer fee, so this card best for borrowers who can benefit from both saving on interest and earning cash back rewards.

5 Best Balance Transfer Credit Cards for Bad Credit

Master Your Finances in 2023: Top Balance Transfer Credit Cards

Cut Interest Costs in Half: The Best Visa Balance Transfer Cards of 2023

10 Best 0 APR Credit Cards in 2023

What Else Should You Look For in a Balance Transfer Card?

In addition to a lengthy 0% term and low fees, look for these other key features when comparing balance transfer cards:

- No annual fee - Avoid cards that charge annual fees, which add to your long-term costs.

- Soft inquiry approval - Some issuers provide an initial offer displaying your 0% term length and credit line via a soft credit inquiry before you formally apply. This helps avoid unnecessary hard inquiries that can impact your credit score.

- Interest-free financing plans - Cards like Citi Flex Loan and Wells Fargo Reflect allow you to finance large purchases over a fixed term at 0% when you meet minimum purchase requirements. This can provide an affordable alternative to balance transfers for big expenses.

- Perks - Some cards offer additional perks like cash back, travel rewards, purchase protections, credits, or access to cardholder discounts. Consider cards that provide added value aligned with your spending habits.

What’s the Best Transfer Strategy with Balance Transfer Cards?

First, focus on paying off cards charging the highest interest rates to maximize savings on expensive interest charges. Avoid repeatedly transferring the same balances across multiple cards, as this accumulates fees over time without actually paying down any debt.

Stick to transferring only an amount you can comfortably pay off within the card’s intro 0% term period. Consistently making at least the minimum payment is essential as well. Otherwise deferred interest often kicks in, meaning you retroactively owe interest on the original balance going back to the account open date.

Ideally use your monthly savings from reduced interest to pay down the transferred balance faster during the intro period. This can help you become debt-free even quicker.

Frequently Asked Questions (FAQs) About Balance Transfers

How long do balance transfers take?

Depending on the issuer, balance transfers may take several weeks to complete. To make the most of the months you enjoy interest-free credit, try asking for transfers as soon as your account is opened.

What credit score do you need for balance transfer cards?

To approve balance transfer card applications, most banks require a credit score in the 670+ area, which is considered outstanding or excellent. For those with fair credit scores between 640 and 669, a few issuers provide balance transfer choices; however, approved credit limits are typically smaller.

Can a balance transfer hurt your credit score?

Your credit scores may be somewhat impacted by opening a new card for a balance transfer since it results in a hard inquiry and a decrease in the average age of your accounts. On the other hand, paying your bills on time and using the card sensibly shows good conduct that promotes good long-term credit.

Should I take out a personal loan to consolidate debt instead?

Although you can combine several sums into a single fixed-rate monthly payment with a personal loan, even the finest personal loans now have interest rates that are more than 15% on average. With balance transfer cards, you can pay off debt temporarily interest-free before the regular purchase APR kicks in. The cards also offer shorter term 0% financing.

What types of debt are eligible for balance transfers?

The majority of credit card companies allow balance transfers from major issuer credit cards. Under specific conditions that differ from provider to provider, several lenders permit transfers from retail cards, auto loans, student loans, home equity debt, and personal loans.

The Bottom Line

A balance transfer credit card presents an effective strategy to reduce interest expenses and pay off credit card balances faster. Take advantage of historically long 0% intro APR offers from top issuers like Wells Fargo and Citi using our guide if you have good credit.

Focus on making payments on time during the intro period while concentrating any freed-up cash toward paying down your principle balance. This disciplined approach helps ensure you logout debt-free without accumulating any deferred interest penalties

Really useful information 😊 please share more articles with us.